Same BatchBacktesting engine as the earlier indicator experiment, but emphasized at portfolio scale: many tickers, two strategies, equities plus crypto, aggregate winners and losers. Version française.

Why run many tickers at once

Single-ticker backtests flatter you. A grid run answers:

- Does this rule only work on one heroic symbol?

- Are disasters clustered in a sector or era?

- Is crypto dominating the leaderboard because volatility is unbounded in the sim?

Architecture (same as BatchBacktesting)

| Layer | Role |

|---|---|

| Data adapters | FMP + Binance fetch |

| Strategy objects | EMA, MACD parameter sets |

| Runner | Thread pool, CSV output, optional plots |

output/ | Per-run artifacts — not committed to GitHub by default |

Pre-calculated results are not in the upstream repo (too user-specific). You generate locally, then inspect output/charts/....

Running at scale

run_backtests(get_SP500(), strategy=EMA, num_threads=12, generate_plots=True)

run_backtests(get_SP500(), strategy=MACD, num_threads=12, generate_plots=True)

run_backtests(get_all_crypto(), strategy=EMA, num_threads=12, generate_plots=True)

run_backtests(get_all_crypto(), strategy=MACD, num_threads=12, generate_plots=True)

Tune num_threads to your machine and API rate limits.

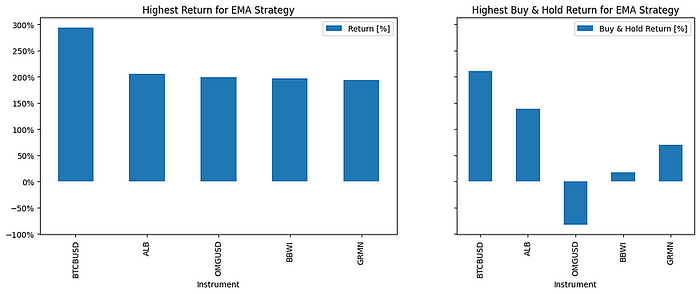

Reading leaderboard extremes (EMA example)

High returns often mix:

- Long bullish windows on leveraged crypto pairs.

- Mean-reversion false signals in sideways stocks (sometimes lucky).

- Parameters tuned implicitly by the default strategy class.

Deep negatives flag:

- Illiquid symbols where the sim still trades.

- Trend rules in collapsing sectors.

- Stablecoins or broken pairs treated like normal tickers.

Before narrating “MACD beats EMA,” compare median return, not only top decile.

Honest limitations

- Not financial advice.

- Fees, borrow, halts, and corporate actions are only as good as the data feed + library defaults.

- Past batch output ≠ future edge.

Takeaway

Use multi-ticker backtests as smoke tests for rules — find where they break, not where to deploy capital.

Related posts

Originally published on Medium. Full code listings: BatchBacktesting.