I batch-ran EMA and MACD strategies across many tickers with BatchBacktesting — FMP for equities, Binance for crypto. This post explains what the runner does, how to read outrageous leaderboard rows, and why that is not a live trading system. Version française.

What BatchBacktesting is

A Python project that:

- Pulls OHLCV via Financial Modeling Prep (S&P list) or Binance (crypto list).

- Applies a strategy class (EMA or MACD) per ticker.

- Writes CSV + optional HTML charts under

output/.

It is a screening hammer, not a portfolio manager.

Install and run (sketch)

pip install numpy httpx rich backtesting pandas_ta

from batch_backtesting import run_backtests, EMA, MACD

tickers = get_SP500()

run_backtests(tickers, strategy=EMA, num_threads=12, generate_plots=True)

run_backtests(get_all_crypto(), strategy=MACD, num_threads=12, generate_plots=True)

Exact imports and API keys live in the GitHub README — do not commit keys.

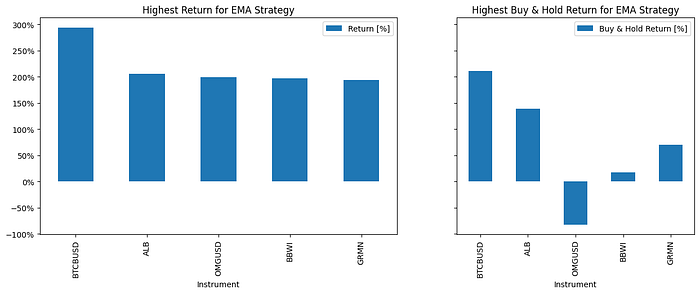

Interpreting example leaderboard rows

From an EMA batch (illustrative):

| Ticker | Return | Gut check |

|---|---|---|

| BTCBUSD | +293% | Crypto volatility + parameter fit |

| BTTBUSD | -99% | Penny-style blow-up — liquidity not modeled |

| UAL / NCLH | deep negative | COVID-era windows punish naive trend rules |

Top and bottom lists are diagnostics, not buy/sell lists. Always open the per-ticker chart (example AAPL chart) before storytelling.

What the Medium import left out on purpose

The original article embedded long pasted code blocks for every helper — maintenance belongs in the repo, not this Hugo page. For:

- HTTP helpers, threading, CSV writers → see

BatchBacktestingsource. - Full French walkthrough → Medium canonical URL.

When not to use this

| Misuse | Why it hurts |

|---|---|

| Deploy top row ticker live | Overfit to window |

| Ignore fees/slippage | Backtest inflates |

| Skip out-of-sample dates | Regime change breaks rule |

Takeaway

Batch runs teach distribution of outcomes under a dumb rule — invaluable for humility, dangerous as autopilot.

Related posts

- Multiple indicators backtesting — scaled leaderboard version

- MarketWatch Python — paper trading API

- Monte Carlo risk bands

Originally published on Medium.